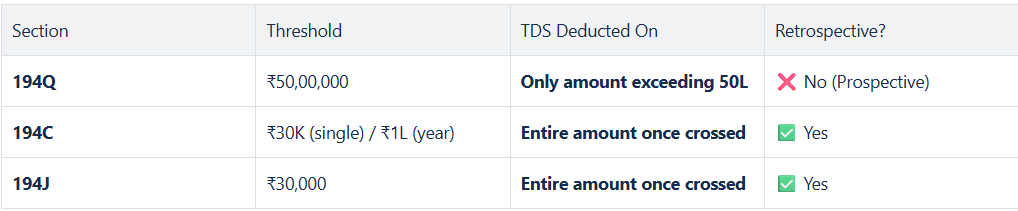

Typically, all TDS sections include an amount slab, and if this limit is exceeded, TDS must be deducted from the very first rupee. This is why, in NetSuite, we check the Retrospective Check box. However, in the case of TDS Section 194Q, retrospective TDS deduction is not necessary; instead, deduction is required only on the amount exceeding the slab limit.

🔷 Section 194Q – Prospective (on EXCESS only)

- Applicable when purchases from a seller exceed ₹50,00,000 in a financial year.

- TDS is deducted at 0.1% on the amount exceeding ₹50L only.

📌 Example:

You purchase from Vendor X:

- April – ₹20L

- June – ₹30L

- Total = ₹50L → no TDS

- In July – ₹5L more → total = ₹55L

- TDS is 0.1% of ₹5L = ₹500 only

- ✔ Past ₹50L is not affected.

✅ This is prospective — deduction starts only after ₹50L, and only on the excess.

🔷 Section 194C – Retrospective in Practice

- TDS is to be deducted:

- If single payment > ₹30,000, or

- If aggregate in FY > ₹1,00,000

- Once this threshold is crossed, TDS is deducted on the entire amount, not just the excess.

📌 Example:

You paid a contractor:

- ₹25,000 in April – no TDS

- ₹25,000 in May – no TDS

- ₹25,000 in June – no TDS

- ₹30,000 in July → Total = ₹1,05,000

🔁 Once it crosses ₹1 lakh:

- TDS is deducted on entire ₹1,05,000, not just on ₹5,000.

✅ This is retrospective — TDS now applies on the entire amount paid so far once threshold is crossed.