In the realm of project management, keeping tabs on project progress, costs, and schedules is crucial for success. This is where Earned Value Management (EVM) comes into play. EVM is a systematic approach that integrates scope, schedule, and cost to provide a clear picture of a project’s performance. Let’s delve into the key components and benefits of EVM.

At its core, EVM is a technique for measuring project performance. It allows project managers to assess a project’s progress objectively by comparing planned performance against actual performance. By doing so, it enables early identification of potential issues and facilitates informed decision-making.

Key Components of Earned Value Management:

- Planned Value (PV):

Planned value is the authorized budget you assign to an activity or work breakdown structure (WBS). This budget doesn’t include a management reserve.

You allocate the planned value in phases over the lifetime of the project. Albeit, at a given point in time, planned value defines the physical work that you’ve accomplished.

The total PV is also known as performance measurement baseline (PMB), budget at completion (BAC), or more often as Budgeted Cost of Work Scheduled (BCWS).

You can calculate Planned Value (PV) using the relation:

PV= BAC x Planned % of complete.

The following example illustrates the relationship:

A project ABC is planned for 15 months with a budget (BAC) of USD 150,000. If the scheduled percentage of work completed after three months is 20%, the planned value after three months would be:

PV= 150000 x 20% = 150000x (20/100) = USD 30,000

PV is also a useful tool for calculating Scheduled Performance Index (SPI) and Schedule Variance (SV)

- Earned Value (EV):

EV is a measure of work performed or the budget authorized for that work. In other words, it’s the budget authorized for completed work. The value of EV cannot be greater than the authorized PV budget for a component.

Since EV calculates the percentage of the project you’ve completed, you’ll measure it with reference to the progress measurement criteria established for each WBS component.

EV is also referred to as Budgeted Cost of Work Performed (BCWP).

To calculate EV, you’d use the relation:

EV = % of work performed/completed x BAC

The following example throws more light on calculating the EV.

A project ABC is planned for 15 months with a budget (BAC) of USD 150,000. The scheduled percent of work completed after three months is 20%. The work completed after the third month is 25%, and the amount spent is USD 30,000. The EV of the project is:

EV= 25% x $150,000 = (25/100) x 150,000 = $37,500

Here, you need not focus on the amount spent. You require only the percentage of work completed.

Of all the tools for assessing project performance, EV is the most important. You’ll use it with PV and AC to calculate:

- Cost Performance Index (CPI)

- Scheduled Performance Index (SPI)

- Cost Variance (CV)

- Schedule Variance (CV)

- To Complete Performance Index (TCPI), and

- Estimate to Completion (EAC).

- Actual cost (AC)

Actual Cost is the realized cost incurred for the work performed on an activity during a specific time period. In other words, the cost you incur while accomplishing the work for which EV is measured.

You measure AC as it relates to PV (budgeted) and EV (measured), but this has no upper limit. whatever you spend to achieve the EV will be measured.

AC is also referred to as the Actual Cost of Work Performed (ACWP). You don’t need the formula to calculate AC because it’s the actual amount spent on performing the planned work, which is illustrated in the following example.

A project ABC is planned for 15 months with a budget (BAC) of USD 150,000. The three months have already passed now, the total amount spent during the period is USD 40,000, and 15% of the work has been accomplished during these months.

From the above case, we can easily note that AC after three months is USD 40,000, and the percentage of work completed is 15%.

If you review the case closely, it is evident that AC ($40,000) is more than PV ($30,000). What this implies is that the project has consumed more budget than planned, so it over-budgeted.

Also, note that the project is trailing against the planned percentage of completion. Instead of 20% complete, it has achieved only 15% work completion. So, the project is behind schedule too.

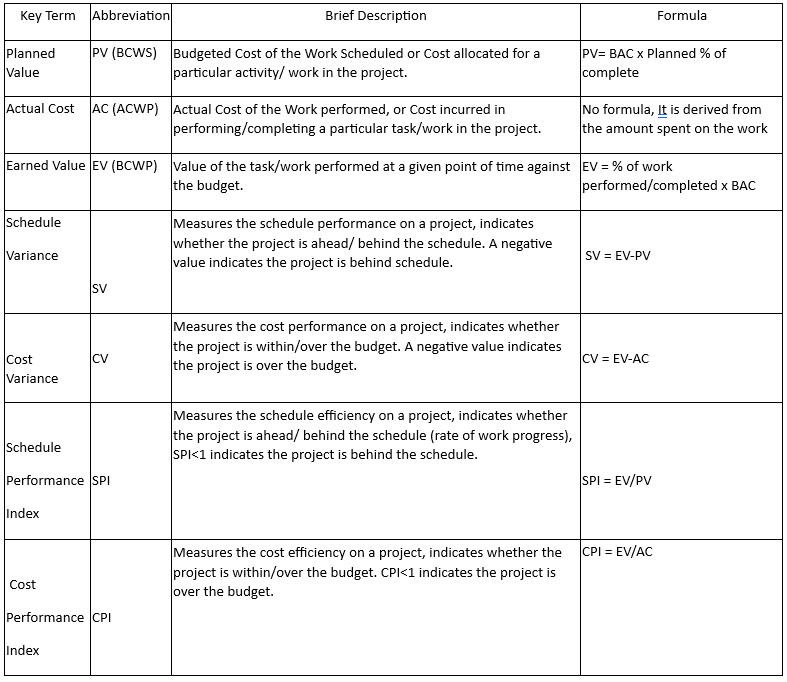

You’ll find some of the formulae in the table below:

Benefits of Earned Value Management:

- Early Warning System: EVM serves as an early warning system, enabling project managers to identify potential cost and schedule variances before they escalate.

- Objective Performance Measurement: By quantifying project performance using EV, PV, and AC, EVM provides an objective assessment of project health, fostering transparency and accountability.

- Data-Driven Decision Making: EVM equips project managers with actionable insights derived from quantitative data, facilitating informed decision-making and effective resource allocation.