A Letter of Undertaking (LUT) under India’s Goods and Services Tax (GST) is a document allowing exporters to export goods or services without immediately paying the Integrated GST (IGST). It acts as a pledge from the exporter to meet all export obligations and follow GST regulations.

Purpose and Benefits

- The main advantage of an LUT is that it prevents an exporter’s working capital from being tied up in the tax refund process. Key benefits include:

- Tax Exemption: Enables “zero-rated” supplies without requiring IGST payment upfront.

- Improved Cash Flow: Helps maintain better financial liquidity for business operations.

- Simplified Process: Avoids the need for complicated tax refund procedures.

- Global Competitiveness: Allows for more competitive pricing in international markets.

Eligibility Criteria

Most registered taxpayers involved in exporting goods or services can file an LUT. A key requirement is that the exporter must not have been prosecuted under the CGST or IGST Act (or any previous law) for tax evasion exceeding ₹2.5 crore.

If an exporter is not eligible for an LUT, they are required to provide an export bond, often involving a bank guarantee.

Validity

An LUT is valid for one financial year from the date it is submitted. Exporters need to file a new LUT each financial year to continue benefiting from tax-free exports. Filing the renewal before the current LUT expires is advisable to avoid operational disruptions.

In India’s GST system, exporters can ship goods without paying IGST upfront if they submit an LUT to the government. This means, instead of paying IGST and then claiming a refund later, you promise (via LUT) that you’ll follow GST rules and export goods properly.

The following are considered as a zero-rated supply under India GST:

- Export of goods or services, or both.

- Supply of goods or services, or both to SEZ (Special Economic Zones).

An exporter dealing in zero-rated goods under India GST can claim a refund as per the following options:

- Export of goods or services, or both, without payment of IGST under LUT (Letter of Undertaking) or Bond. Subject to such conditions, an exporter can claim a refund of the unused input tax credit.

- Export of goods or services, or both, on payment of IGST without any requirement of LUT or Bond. Subject to such conditions, an exporter can claim a refund of the tax paid on goods or services, or both

How does LUT work on NetSuite?

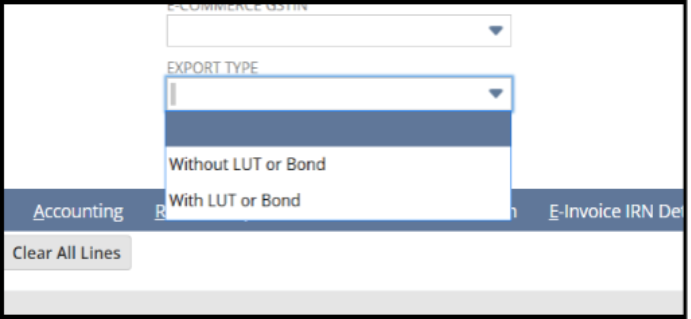

The India Localization SuiteTax Engine SuiteApp enables you to assign an export type to a sales transaction that contains goods, services, or both for export. The SuiteApp calculates GST based on the export type.

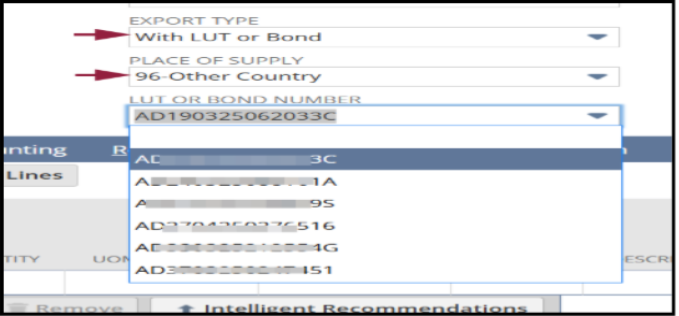

If you choose to export goods or services under LUT or Bond, you can create and assign LUT or Bond Detail records to your export transactions.

On sales transactions, if you set Export Type to With LUT or Bond, IGST is not calculated. However, for tax exemption, the invoice must be approved. If the invoice is not approved, tax is calculated irrespective of applying LUT or Bond.

In NetSuite, when you create an export transaction (like a Sales Order or Invoice for export), the system checks:

- Is this customer/export covered under LUT?

- If yes, then IGST is not applied on the transaction.

- If no, IGST will be calculated and added to the invoice.

Usually, this is controlled by:

- Tax Codes (e.g., “Export under LUT” vs “Export with IGST”)

- Customer or Item Setup (marking them as export eligible)

- Tax Rules in NetSuite’s GST SuiteTax or India Localization bundle.

Impact on Transactions

With LUT:

- The invoice shows 0 IGST.

- Tax code will indicate “Export under LUT”.

- No IGST liability in your GST return for that invoice.

Without LUT:

- IGST is calculated on the invoice.

Impact on IGST Calculations

- LUT basically removes IGST from export transactions.

- In GST reports (GSTR-1, GSTR-3B), exports under LUT are reported separately as zero-rated supplies without payment of tax.

Application Criteria

Criteria 1 – Customer tax registration type: To identify the scenario where the declaration is used, we need to first check the Tax. Registration Type under the Financial subtab in the customer record. The scenarios are only applicable if the registration type is either SEZ or Overseas.

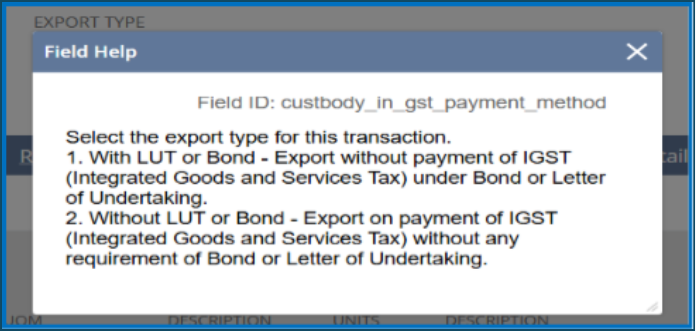

Criteria 2 – Export Type field in Invoice – The Export type in the Invoice will decide which declaration will be applicable.

If the Export Type is ‘With LUT or Bond’, then the Tax amount will be 0.

Declaration to be used – (SUPPLY MEANT FOR EXPORT/SUPPLY TO SEZ UNIT OR SEZ DEVELOPER FOR AUTHORISED OPERATIONS UNDER BOND OR LETTER OF UNDERTAKING WITHOUT PAYMENT OF IGST)

Note: In NetSuite, the rate would be shown as per code, but the amount would be zero. But in the provided sample, the rate and amount are zero. Hence, we might need to set the rate % such that if the invoice export type is with LUT/Bond, then the rate must be 0.

If the Export Type is ‘Without LUT or Bond’, IGST will be charged.

Declaration to be used – (SUPPLY MEANT FOR EXPORT/SUPPLY TO SEZ UNIT OR SEZ DEVELOPER FOR AUTHORISED OPERATIONS ON PAYMENT OF IGST)