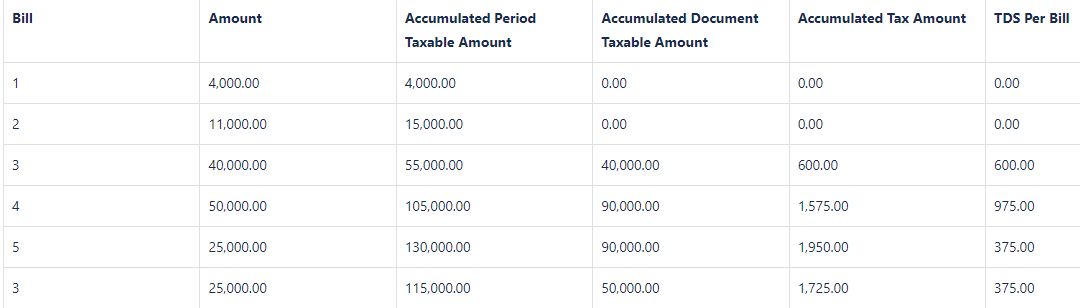

User created Tax Deduction at Source Rule (1.5%) with a Document Threshold of 30,000.00 and Year Threshold of 100,000.00, and wants to know how TDS Liability will be calculated when Vendor Bills with the following amounts are raised:

- Bill 1 = 4,000.00

- Bill 2 = 15,000.00

- Bill 3 = 40,000.00 (changed to 25,000.00 after Bill 5 is raised)

- Bill 4 = 50,000.00

- Bill 5 = 25,000.00

Accumulated Period Taxable Amount is the total amount of Bills raised for a combination of one Customer and one Section Code.

Accumulated Document Taxable Amount is the total amount of Bills raised that met the Document Threshold for a combination of one Customer and one Section Code.

Accumulated Tax Amount is the amount of total Tax charged for a combination of one Customer and one Section Code.

Bills 1 and 2 did not cross the Document and Year Threshold so they would not be charged wit TDS Liability.

Bill 3 is charged by 600.00 (40,000.00 x 1.5%) since Document Threshold was met.

Bill 4 is charged by 975.00 ((105,000.00 x 1.5%) – 600.00) since Document Threshold and Year Threshold was met and 40,000.00 of the total bills raised has been charged with TDS Liability already.

Bill 5 is charged by 375.00 ((130,000.00 x 1.5%) – 1,575.00; or 25,000.00 x 1.5%) since the Year Threshold was crossed and the Year Threshold Amount has been charged with TDS Liability. Since it did not meet the Document Threshold, the amount of Accumulated Document Taxable remains the same.

Bill 3 was changed to 25,000.00 causing the reduction of Accumulated Document Taxable Amount, Accumulated Tax amount, and TDS Per Bill in amount.